Quick Brief — for the hiring manager

The Opportunity

Meta's total compensation package — RSUs, 401(k) matching, HSA, financial coaching stipends — is among the most generous in the industry. Yet a significant portion of employees were not utilizing these benefits effectively, leaving meaningful wealth on the table due to information overload and decision paralysis.

I was brought in to design Paven from the ground up: a mobile-first internal platform that would become the single source of truth for Meta employees navigating their financial lives. The product had to balance complexity with clarity — personalizing a deeply nuanced domain for a highly educated, time-constrained audience.

Full cross-functional build

Illustrators, visual designers, UX researchers, engineers, content managers, CPO, and CEO — zero-to-one launch with no design system to inherit.

End-to-end ownership

Led the entire mobile experience design and served as Lead Designer for the web platform. Set design direction, managed design QA, and partnered directly with engineering on implementation.

Defining the Right Problem to Solve

Before any sketching, I led a structured problem framing exercise with the CPO and CEO to pressure-test our assumptions. The naive framing — "employees need more financial information" — was wrong. Our early research signals pointed to something more nuanced.

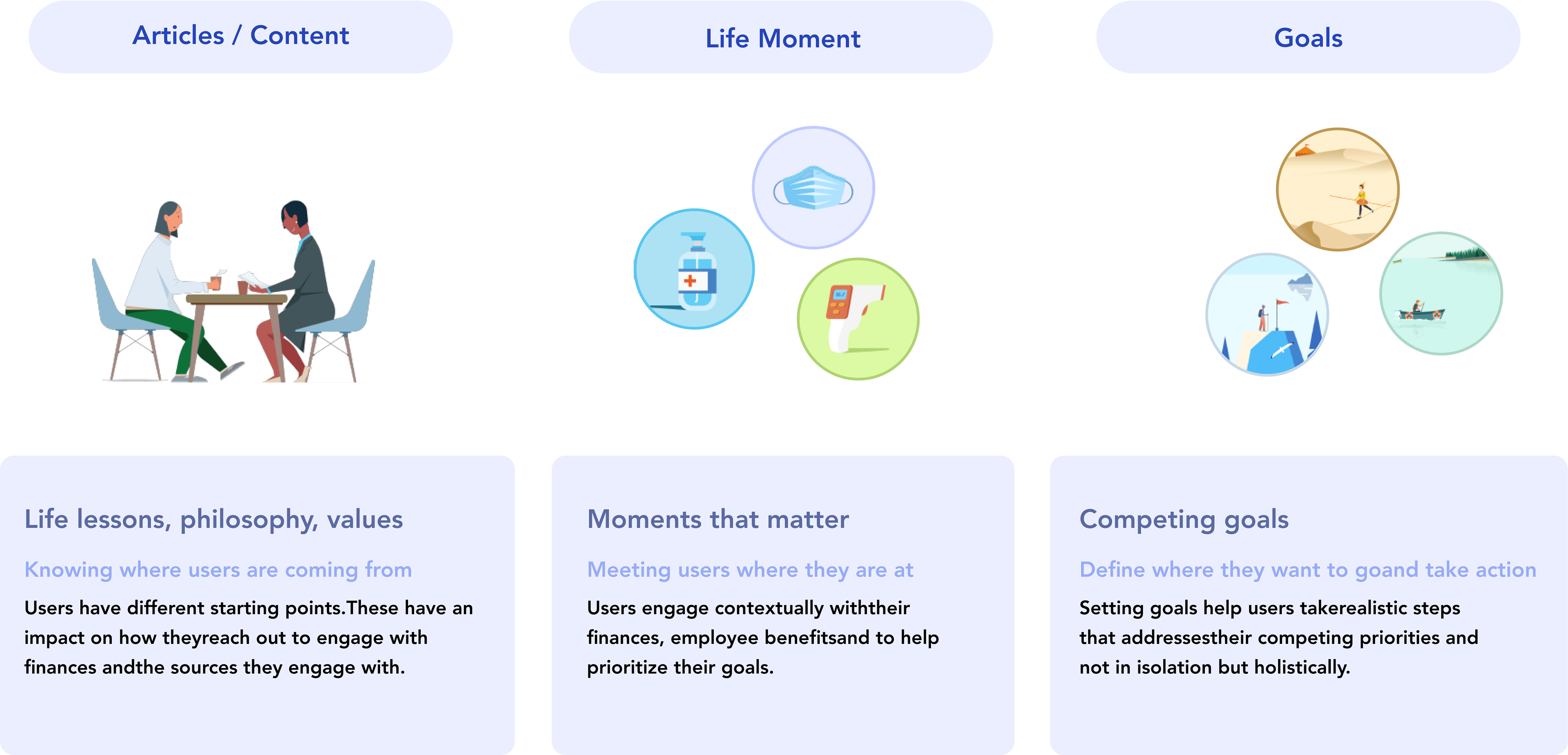

Addressing financial wellness required more than a content hub. Employees needed a platform that combined three distinct capabilities:

Bite-sized, contextualized financial education tied to their specific life stage and benefit eligibility windows.

Intelligent surfacing of relevant content and actions based on user profile, goals, and behavioral signals.

Seamless access to Deloitte financial coaches — without the friction that made scheduling feel like a burden.

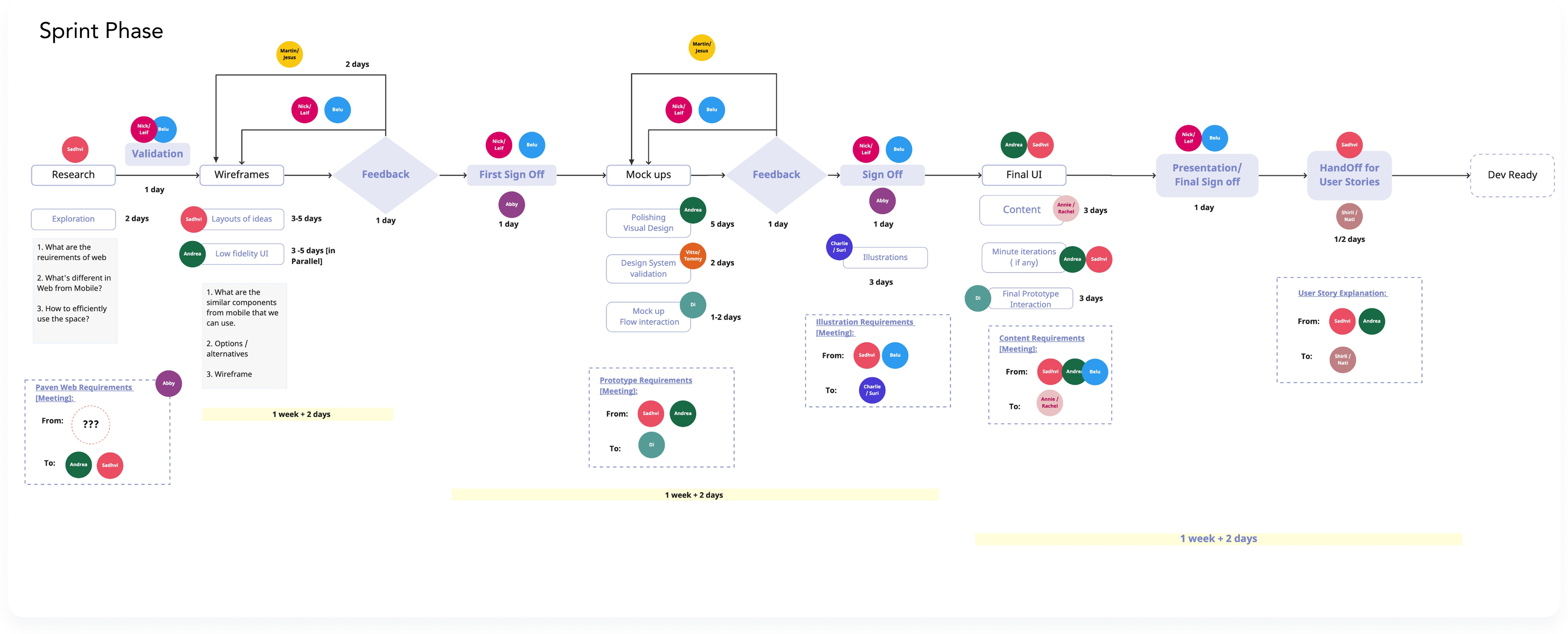

Design Process

A Multi-Method Research Program

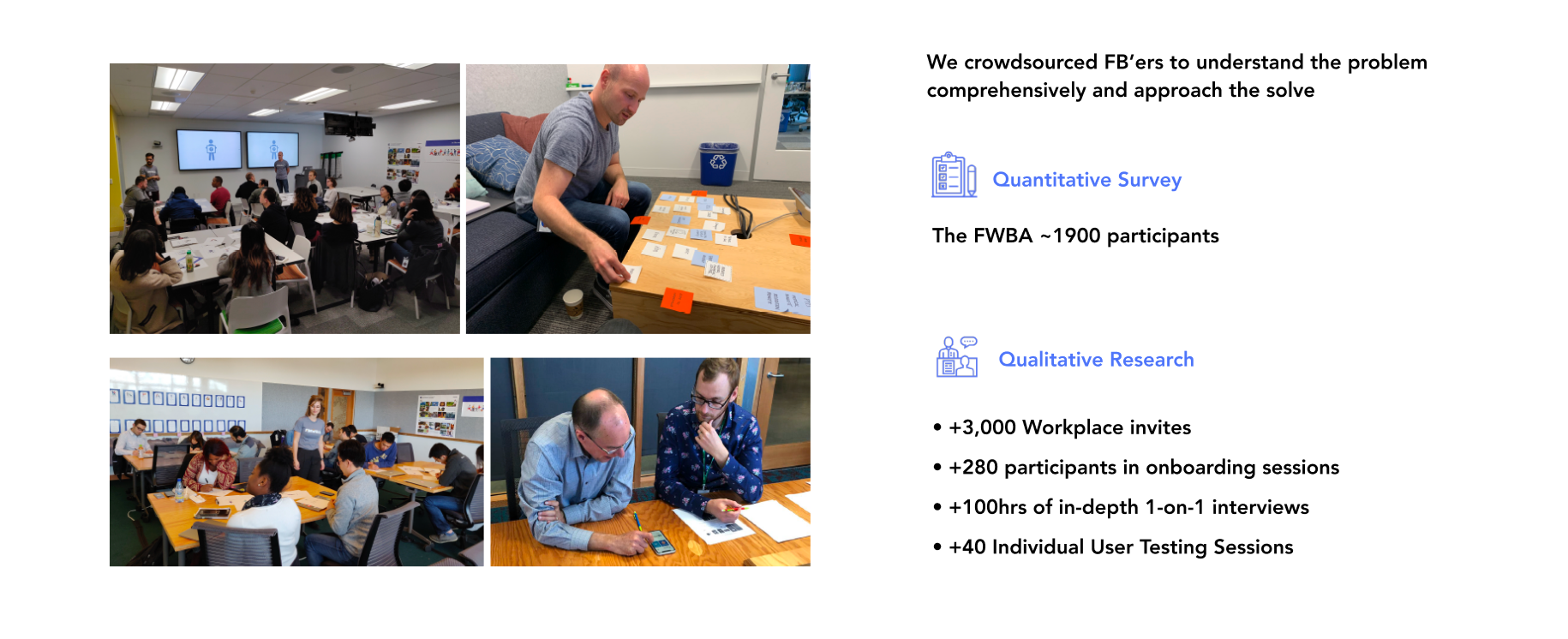

I partnered closely with our UX Research team to design a research program that would give us both breadth and depth. Rather than defaulting to a single method, we ran parallel tracks to triangulate findings across behavioral, attitudinal, and contextual data.

We structured our research around two foundational questions that governed all data collection and synthesis:

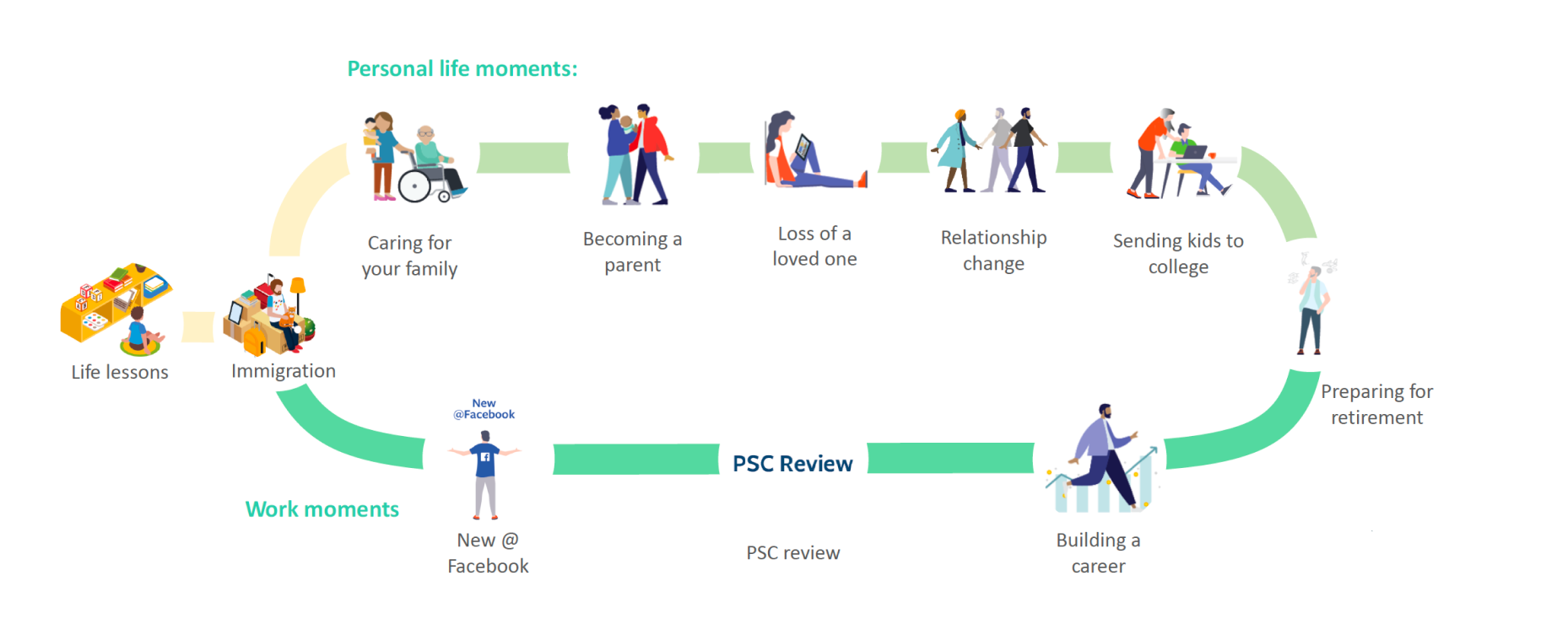

Identity & Life Context

When and in what life scenarios do employees make financial decisions? What life events trigger financial action — or inaction?

Behavior & Decision-Making

How do employees make financial decisions? Where do they seek knowledge? What tools, if any, do they trust?

Methods Deployed

| Method | What We Learned |

|---|---|

| User Interviews (1:1) | Surfaced emotional blockers — shame, overwhelm, and fear of "getting it wrong" were more prevalent than knowledge gaps |

| Journey Mapping | Mapped the full employee financial lifecycle, revealing 6 critical inflection points where users needed support |

| Competitive Analysis | Identified white space: no existing tool bridged financial literacy with personalized human coaching in one experience |

| 2×2 Prioritization | Facilitated cross-functional sessions to prioritize feature bets across impact vs. effort axes |

| Persona Development | Distilled research into distinct user archetypes segmented by financial confidence and life stage |

| Product Provocations | Speculative design concepts pressure-tested assumptions and unlocked non-obvious directions with stakeholders |

| Brainstorming / HMW | Structured "How Might We" sessions translated research tension into design opportunity |

6 Critical Journey Map Insights

- 1Understand where I am by knowing where I came from — employees needed context before they could plan forward.

- 2Defeat the Overwhelm Paralysis — the sheer volume of benefit options caused complete decision freeze.

- 3Avoid the Figuring-It-Out Fatigue — employees were exhausted from researching the same ground repeatedly with no clear answer.

- 4Balance conflicting priorities — short-term needs (student debt, rent) were in constant tension with long-term planning (RSU vesting, retirement).

- 5Engage with true belonging — employees wanted to feel that financial guidance was designed for their situation, not generic advice.

- 6Build resilience and course-correct — employees needed permission and support to adapt plans as life changed.

Key Barriers Identified

From Insight to Feature Bets

With research synthesized, I facilitated structured ideation sessions with our cross-functional team. The goal was to converge on a focused solution space — not a feature laundry list, but a coherent product thesis that addressed the root causes we'd uncovered.

Journey mapping surfaced six core failure modes. From these we defined a solution space that addressed each barrier directly — not with features, but with structural design choices about how content, goals, and coaching should interact.

From this thesis, we converged on Paven's three core feature pillars:

Learn

Curated financial education modules tied to employee life stages and Meta benefit eligibility windows.

Plan

Goal-setting and personalized benefit optimization tools that translate education into concrete action.

Connect

Frictionless access to Deloitte coaching sessions — pre-contextualized by what the user has already learned in-app.

Structuring Complexity

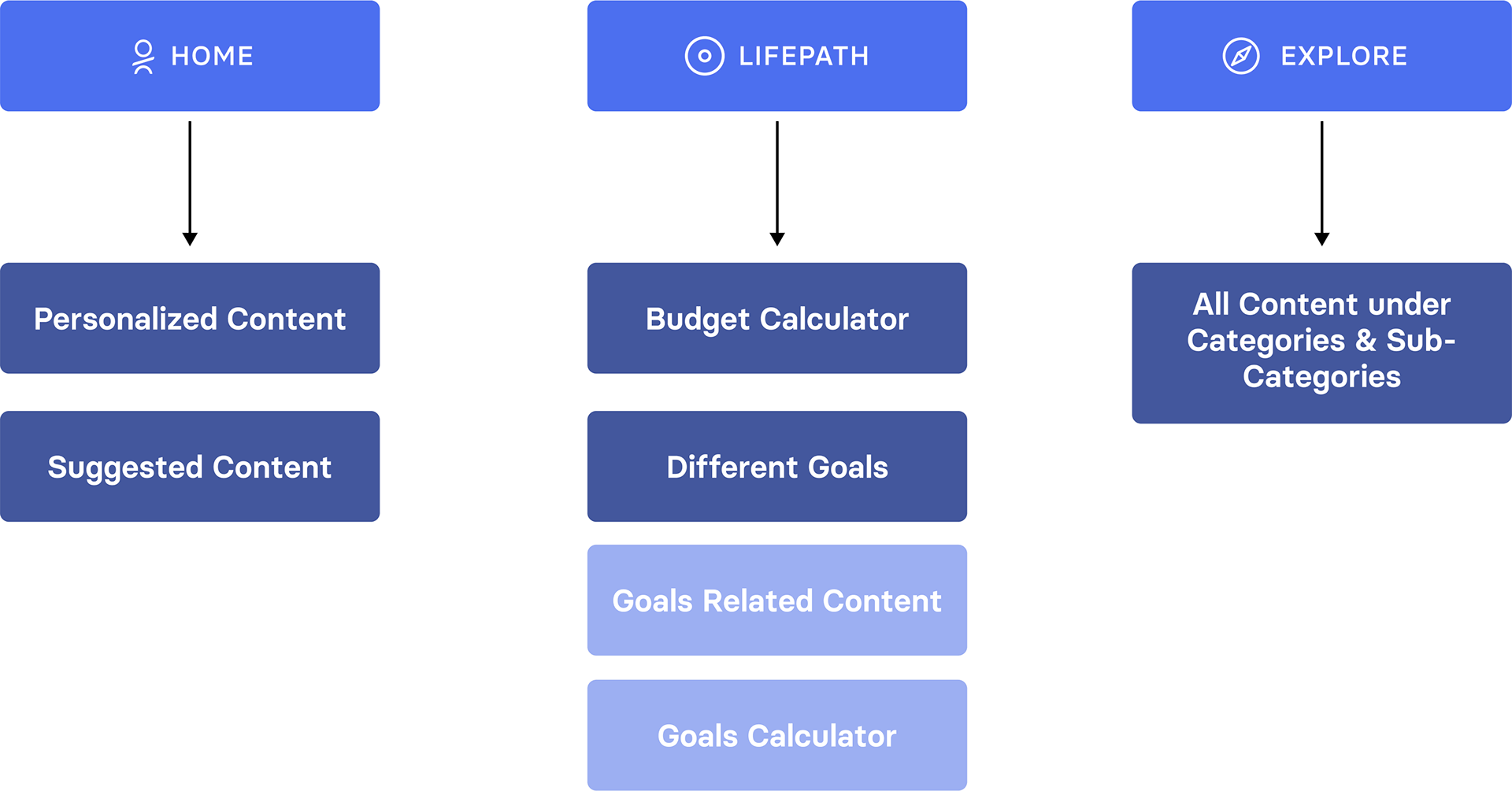

With no existing design system or product to inherit, I architected the information architecture from scratch — three core areas of the app (Home, Lifepath, Explore) — and mapped the full sprint delivery timeline before moving into visual design, ensuring research findings directly shaped IA decisions.

I established four design principles that governed all design decisions across the team and both platforms:

Confidence, not comprehensiveness

Surface the right information at the right moment. Never show everything at once.

Progress over perfection

Celebrate small financial actions to build momentum and counter paralysis.

Human at the center

Technology enables, but human coaching closes the confidence gap. Design the handoff to feel seamless.

Personal, not generic

Every touchpoint should feel designed for this specific employee — not "Meta employees" as a monolith.

Key Design Decisions

"I can control the course of my life (and so I should)"

| Am I spending my time right? | Will I be protected for my future? | Am I moving at the right pace? | Do I have enough information to make the right decision? | |

|---|---|---|---|---|

| User Concerns | Little time to see the bigger picture | Many goals to balance | Uncertainty of progress | Overwhelming financial system |

| Barriers | Freedom from > Freedom to | Reconcile conflicting goals together rather than in isolation | Focus on the now vs. focus on the future | Learn based on financial relevancy to me |

| Solution Space | Enable users to see the big picture and redefine financial wellbeing as "freedom from" to "freedom to" | Reconcile conflicting goals together rather than in isolation | Enable users to reduce their temporal distance between their goals | Learn based on financial relevancy to me |

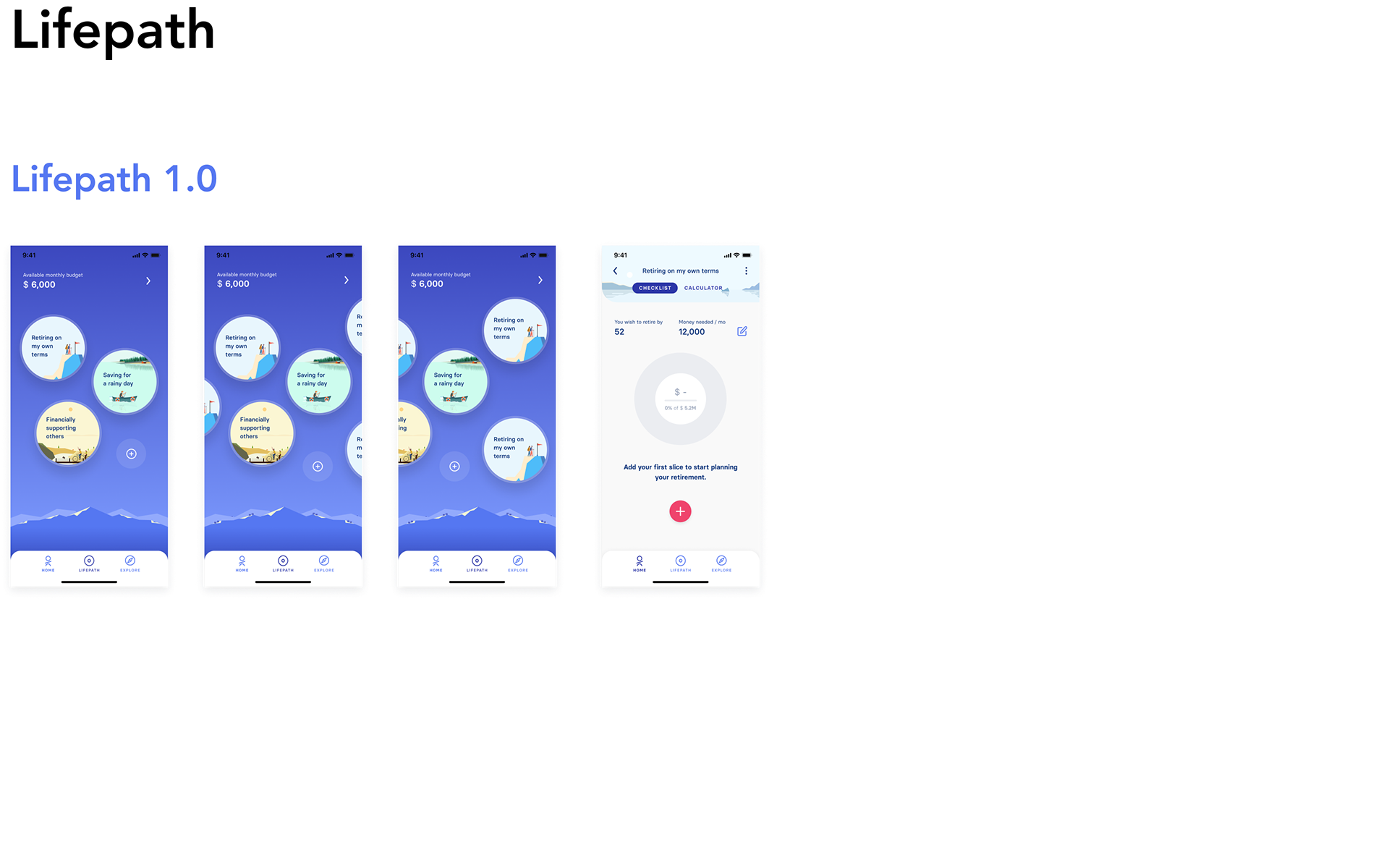

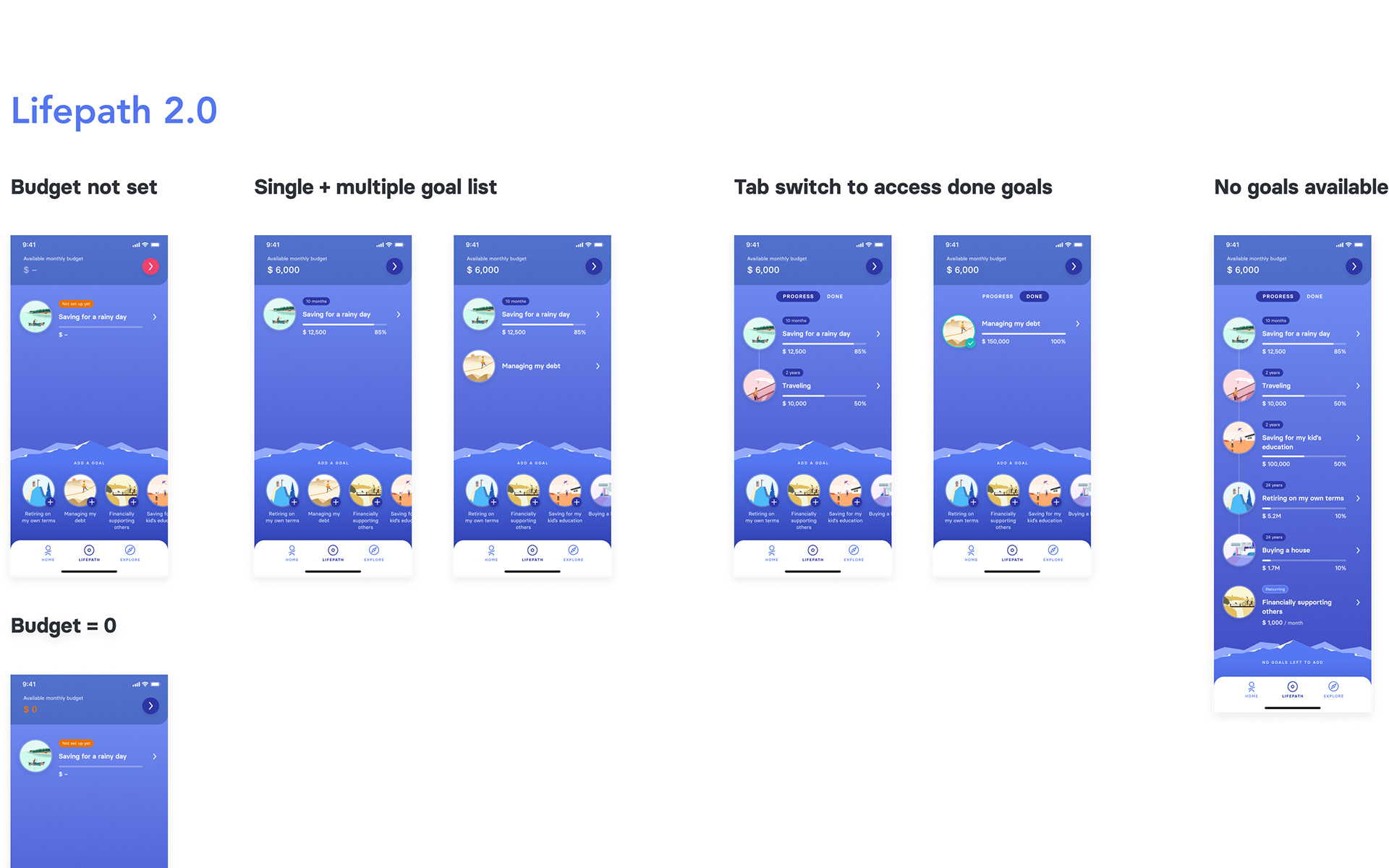

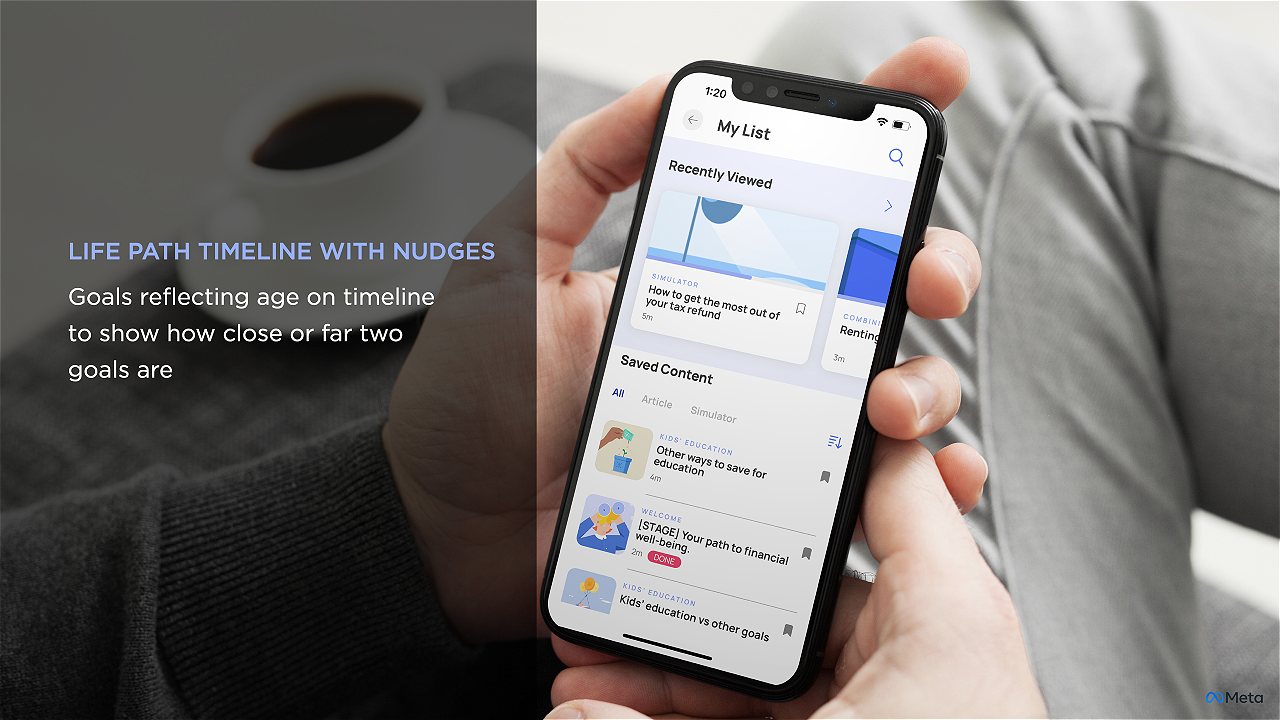

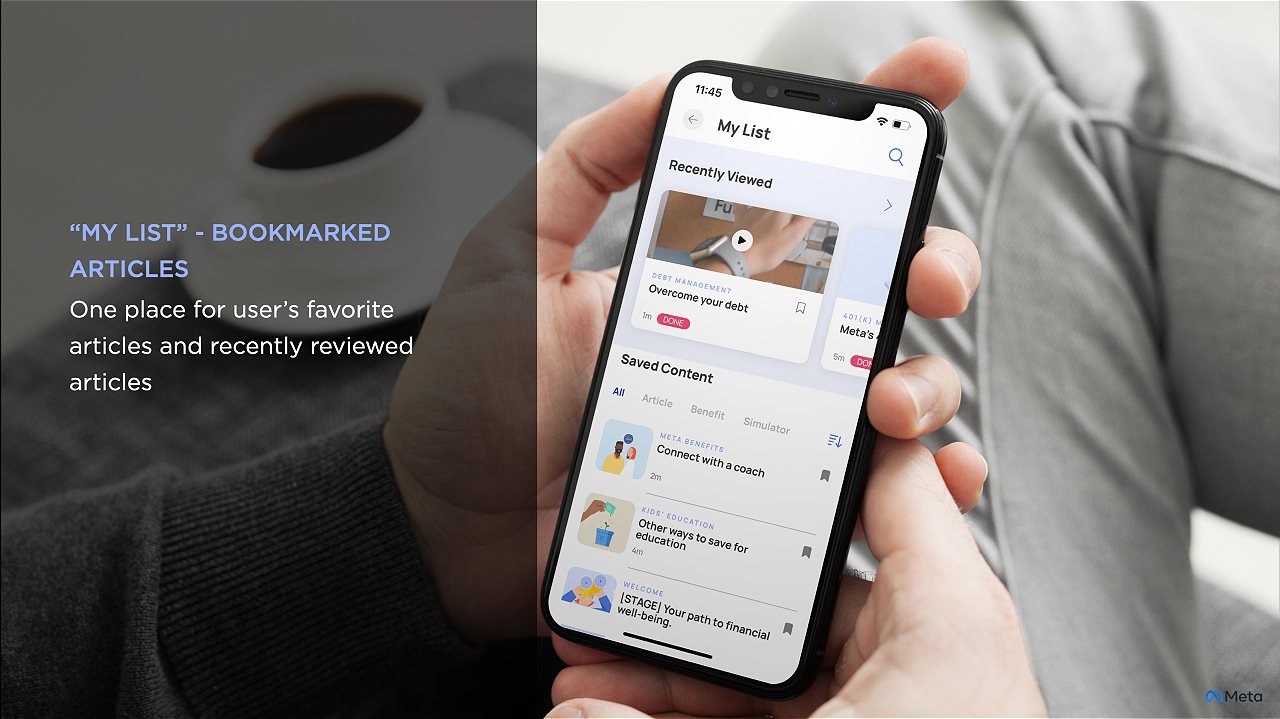

Early Designs — Paven v1 for Facebook Employees

The first version established the core content model — financial articles, goal-setting, and coaching access. Designed exclusively for mobile, the early build validated the product hypothesis before expanding to web.

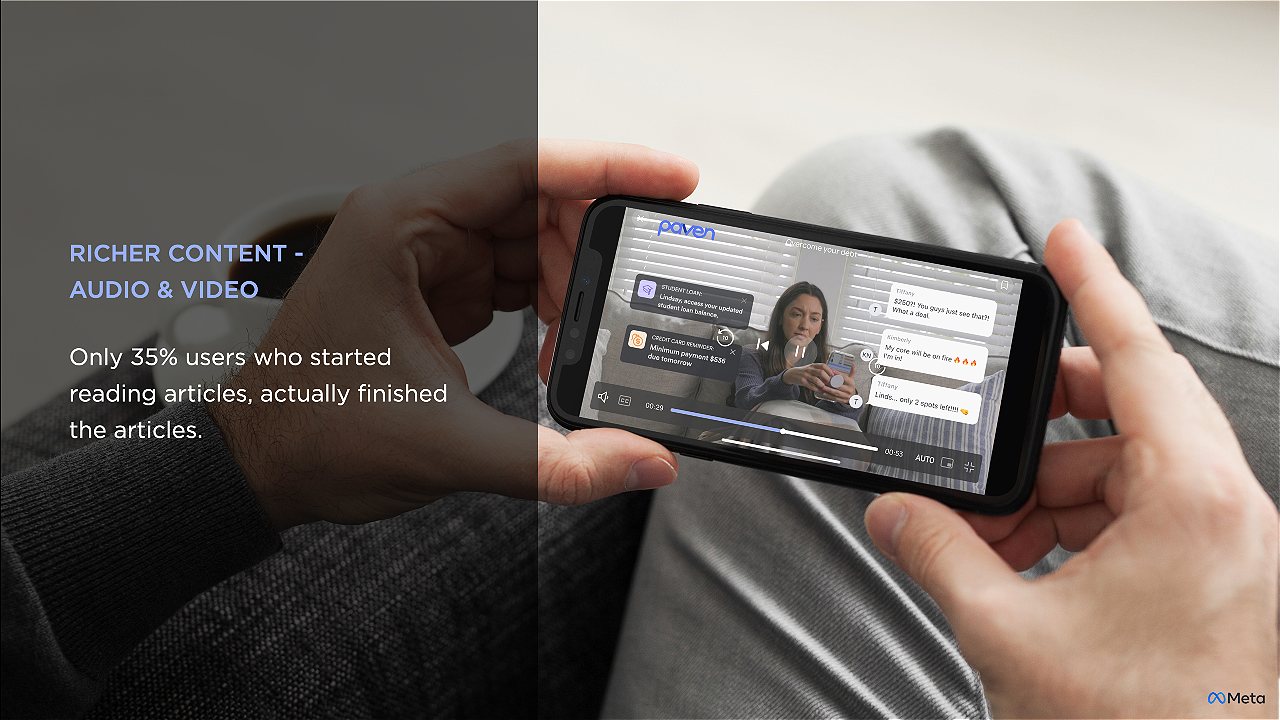

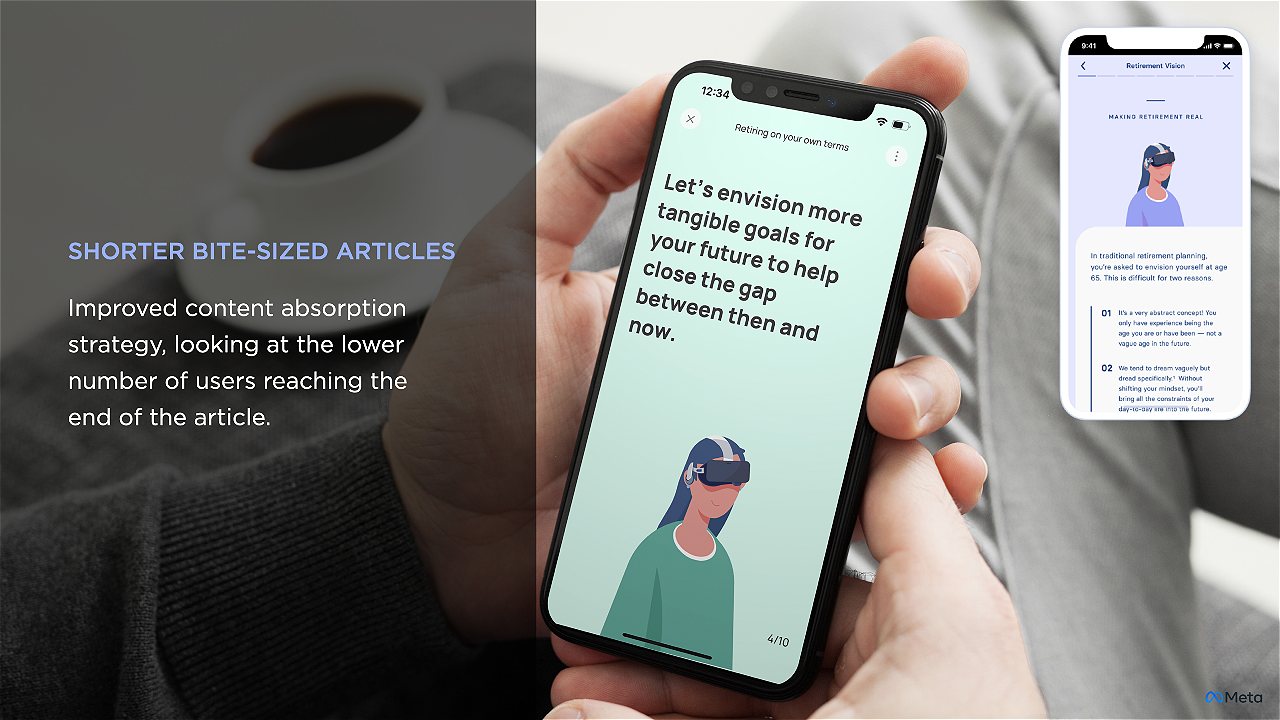

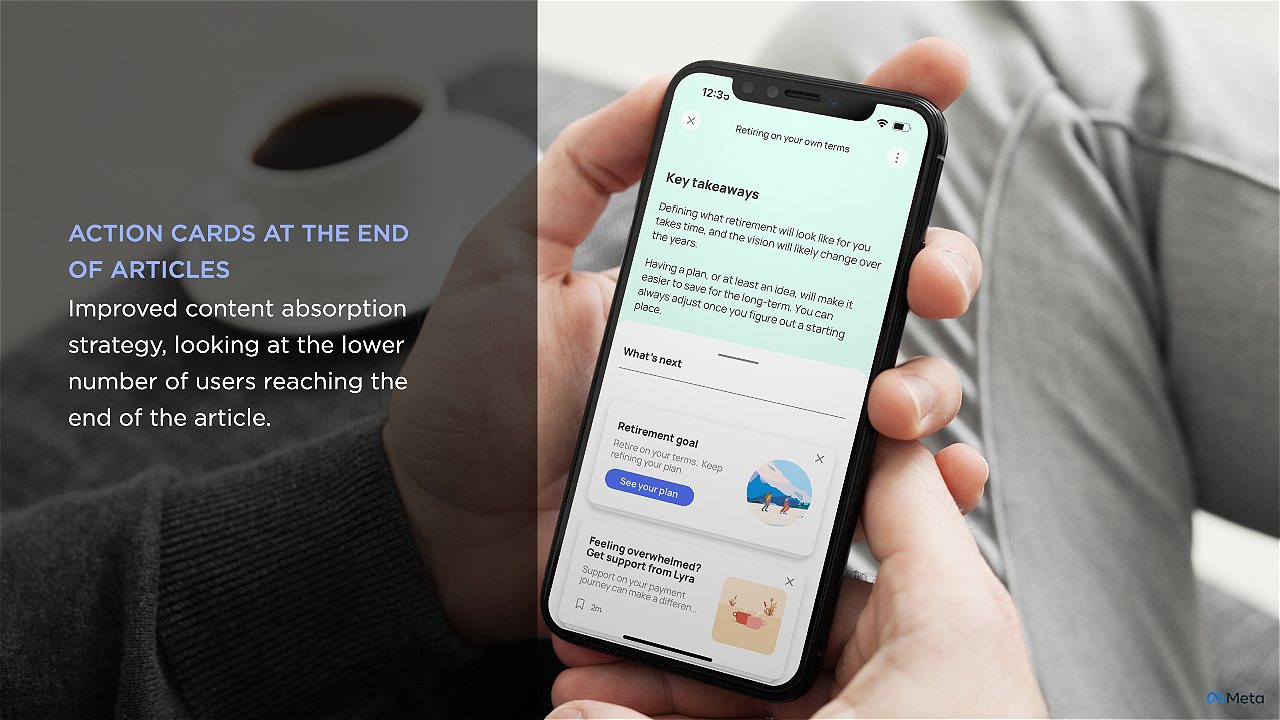

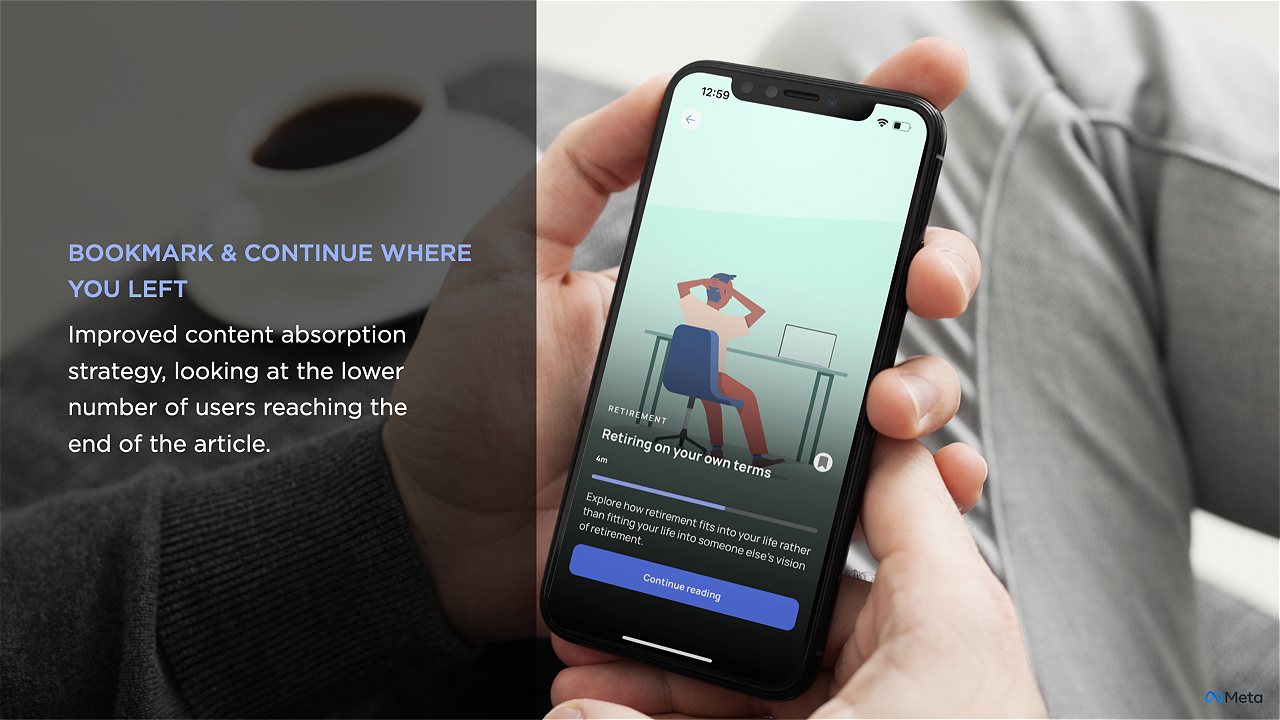

Mobile UX — Solving the Content Engagement Problem

Only 35% of users who started reading articles actually finished them. We redesigned the entire content experience: shorter bite-sized formats, rich audio/video, action cards at the end of each article, and bookmarking — each change driven by a specific observed failure mode.

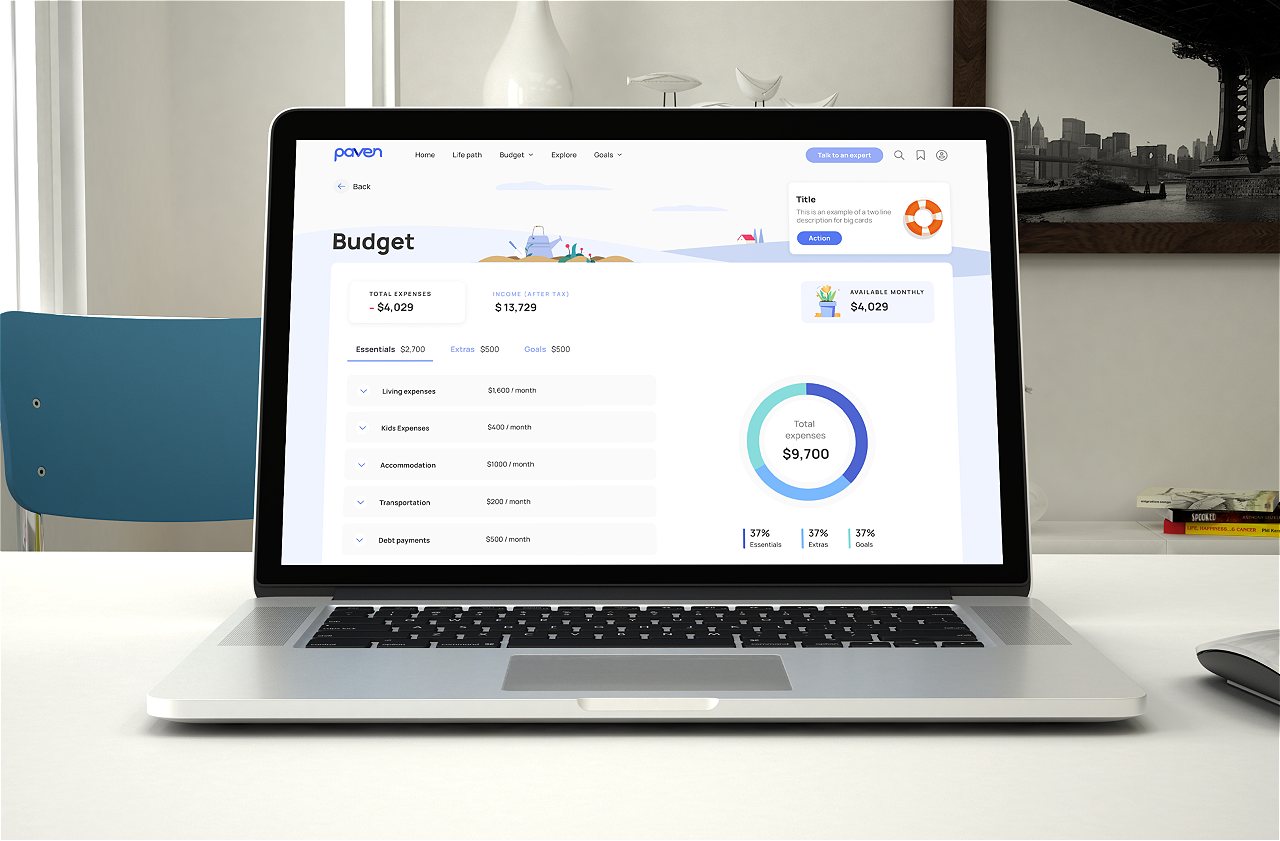

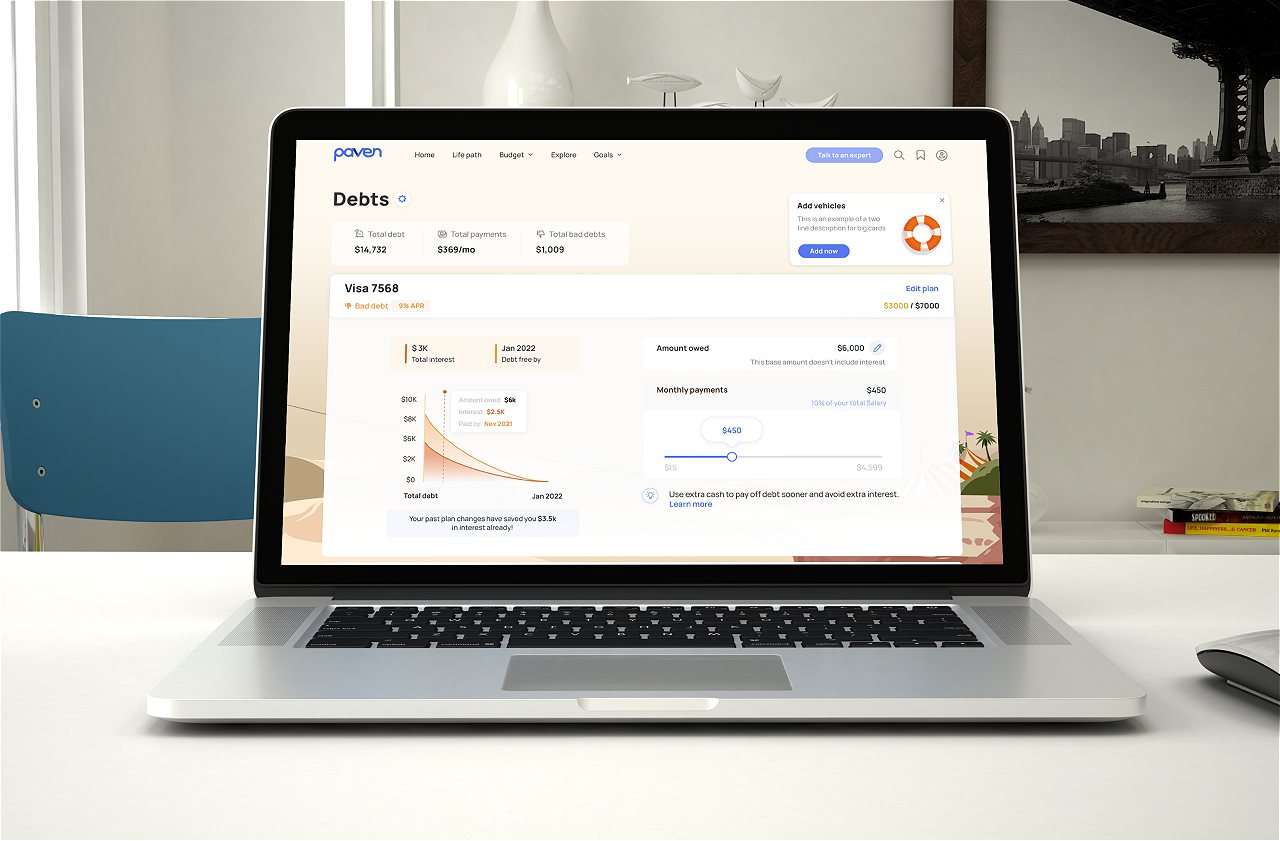

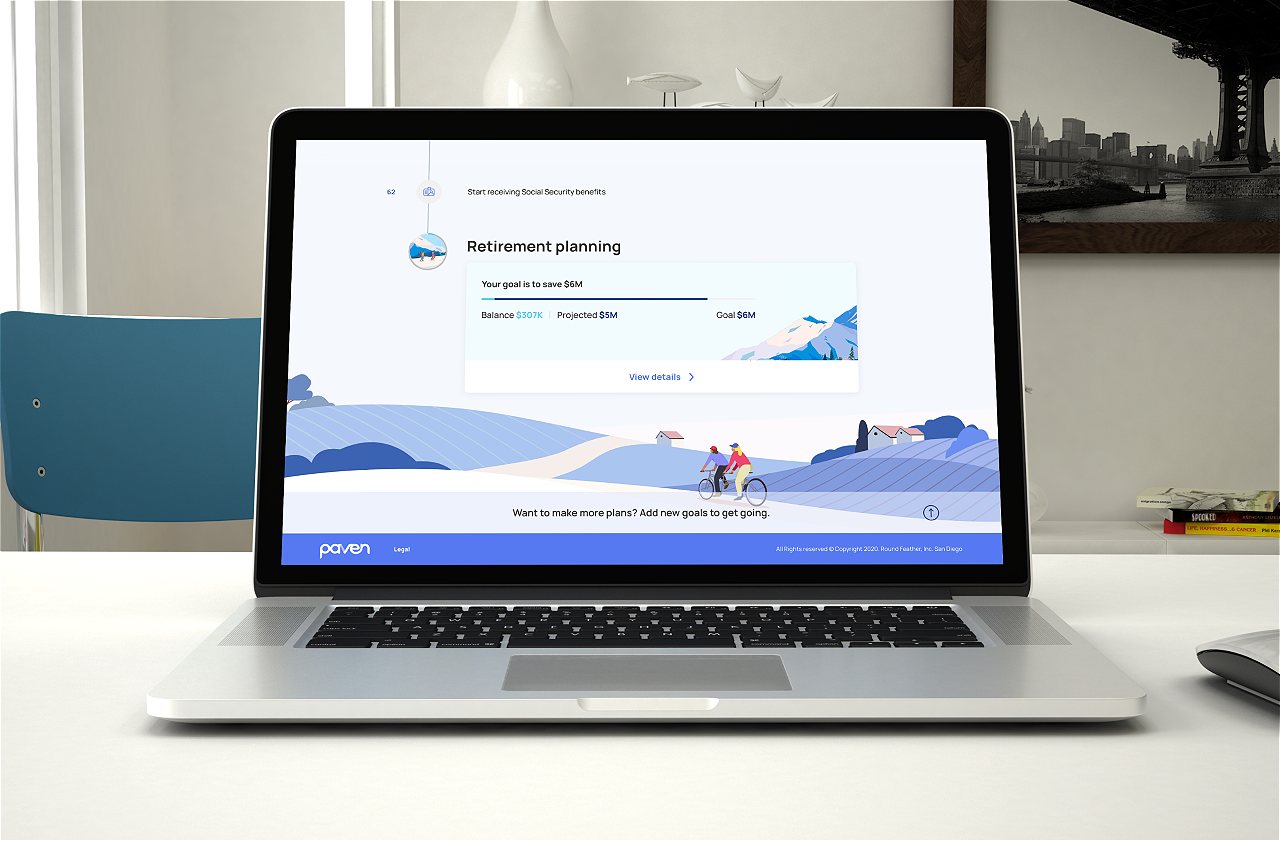

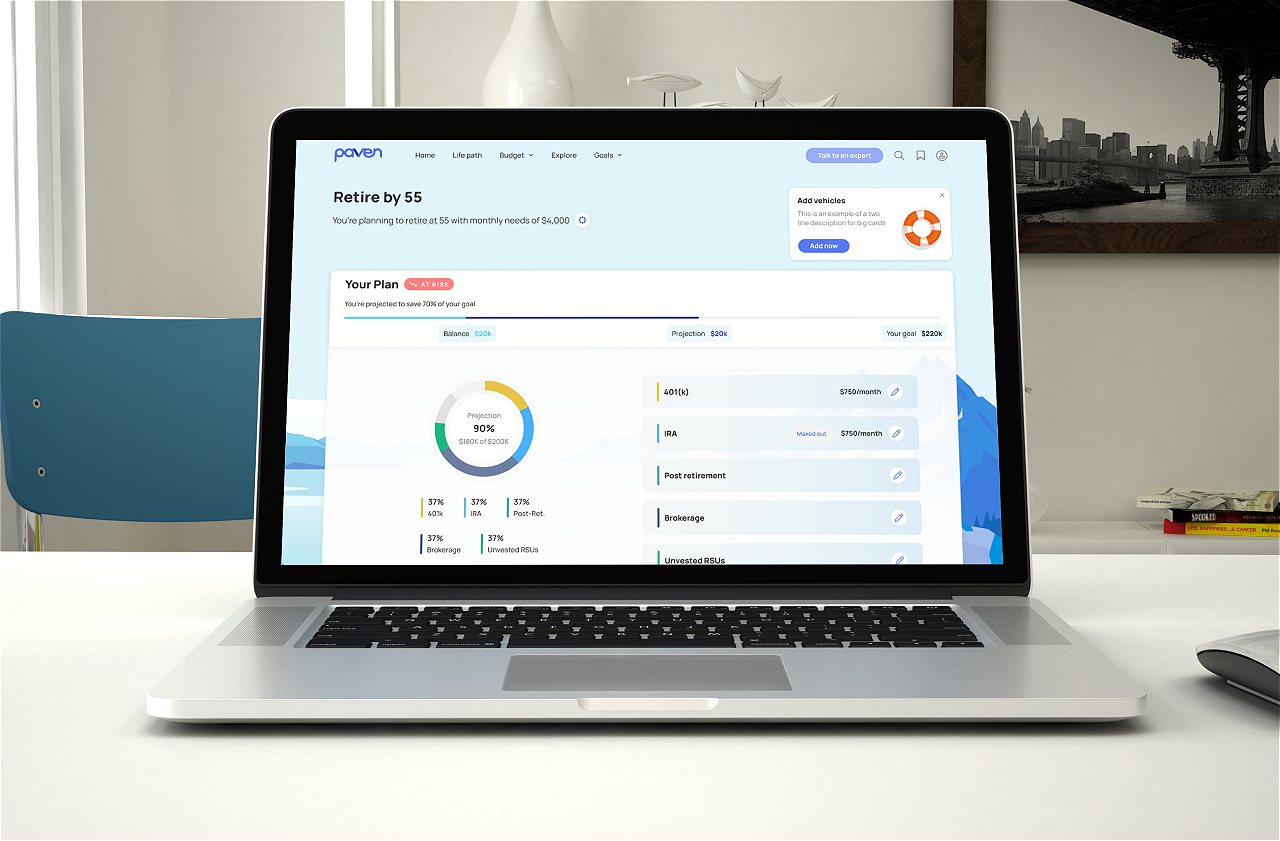

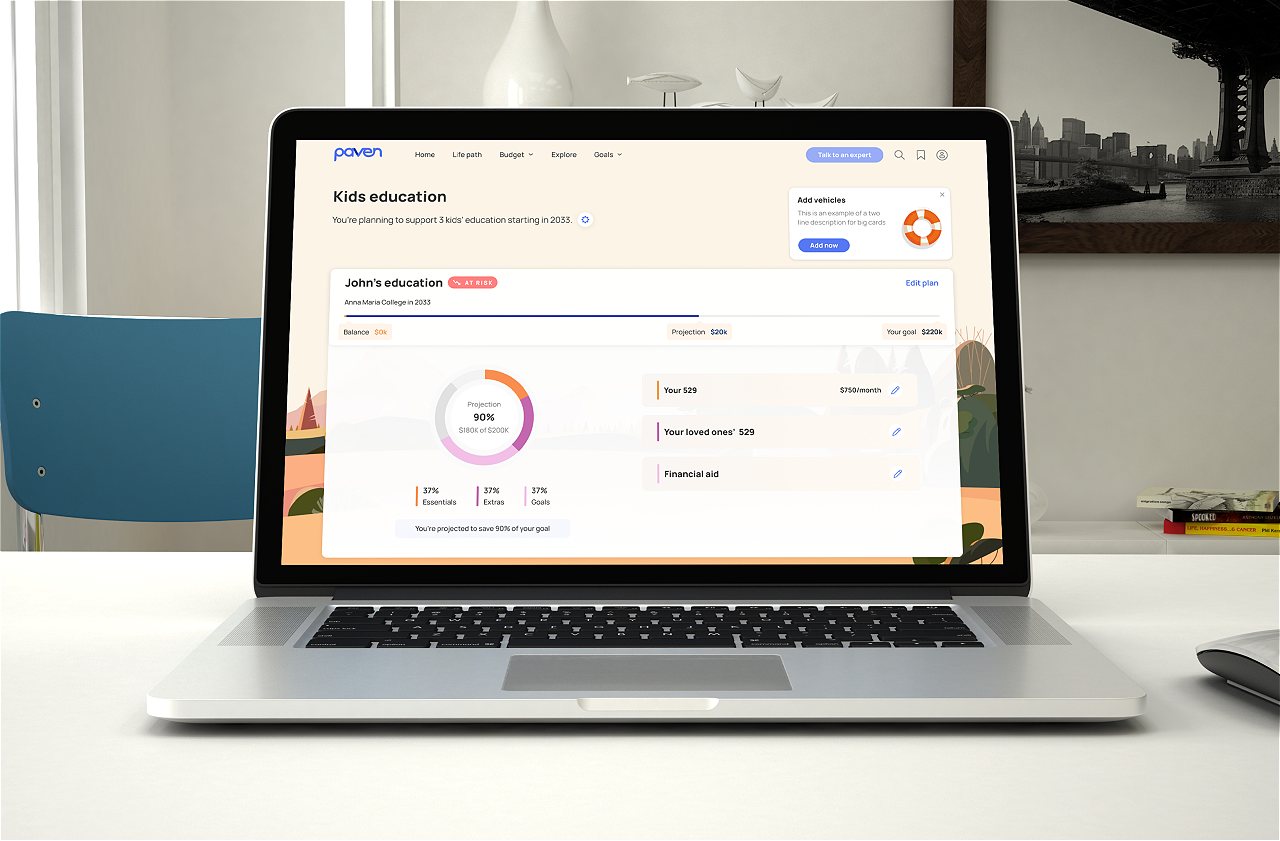

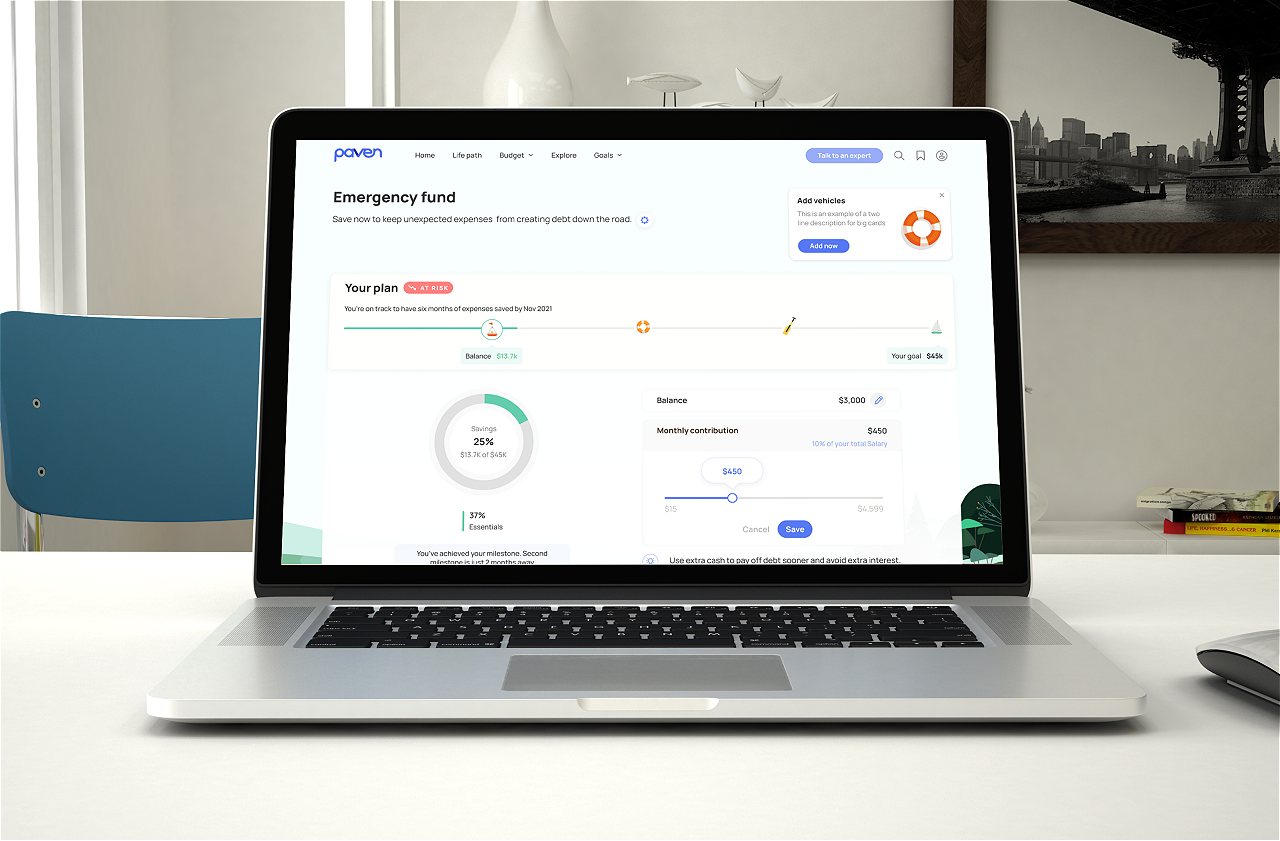

Web Experience — Paven Launched May 2022

The web experience was designed independently from mobile — not stretched, not responsive-scaled. Different context, different density, different user intent. As Lead Designer for web, I had to translate a mobile-first content model to a wider canvas without losing the intimacy and personalization that made mobile work.

Each financial goal gets its own dedicated planning view: budget, debt, retirement, education, and emergency funds modeled with full projection tooling.

Measurable Results

Paven's impact was tracked across user adoption, behavioral change, and direct business value delivered to Meta's partnership with Deloitte. These results validated our design thesis and drove continued investment in the platform.

User base growth from v1 to Paven 3.0 — sustained growth across every major product release.

Of all Deloitte financial coaching sessions now booked directly through Paven — a core engagement KPI.

Product valuation at time of engagement. Better-prepared users reduced per-session Deloitte advisory costs.

Beyond the metrics, Paven shifted how Meta thought about employee benefits. Financial wellness moved from a checkbox item to a product Meta was genuinely proud of — one that measurably reduced employee stress and improved employees' relationship with their own financial future.

Challenges, Reflections & Roadmap

Design challenges we navigated:

Mobile-first at a cost

Illustrations and navigation patterns designed for mobile required significant rethinking for web and iPad. I established a cross-platform design handoff process mid-cycle to avoid costly rework in future releases.

PNG to SVG migration

A content-heavy, illustration-rich app strained load times. I partnered with engineering to define an SVG migration path, trading short-term production complexity for long-term performance gains.

The Next Horizon

Integrating real bank account data directly into Paven — creating a unified financial command center for Meta employees. This requires solving a trust and data privacy design challenge I'm actively working through with research.